Australian shopping centres remain one of the most resilient and attractive real estate investment opportunities in today’s market.

With an economic backdrop shaped by falling interest rates, resilient consumer demand, sustained population growth, elevated construction costs, and limited land supply, existing and centrally located retail assets are well-positioned to capture both long-term income growth and capital appreciation.

In this insight, we examine the structural and cyclical fundamentals underpinning the sector’s positive outlook, and the case for shopping centres in diversified investment portfolios.

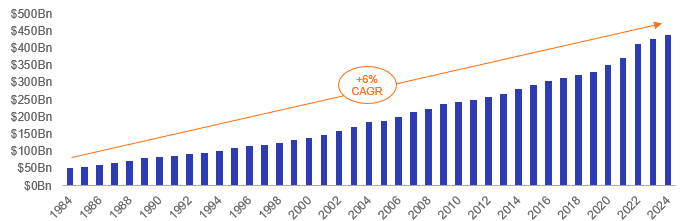

Four decades of unbroken retail sales growth

Australia’s retail sector is underpinned by a strong and proven track record of long-term growth. According to the Australian Bureau of Statistics (ABS), annual retail spending has increased every year for the past 40 years, delivering a compound annual growth rate of ~6%.

Over the last three decades, Australia’s retail expenditure growth has not only been consistent but also outpaced key global peers. Average annual growth of 5.0% compares favourably with the US at 4.5% and the UK at 3.5%, underscoring the sector’s structural strength and international competitiveness.

This resilience has been tested and proven through multiple periods of economic disruption, from the global financial crisis to the COVID-19 pandemic. Even in today’s environment, where inflation and rising living costs are pressuring household budgets, the sector continues to expand. This consistent growth highlights the enduring strength of Australia’s retail sector and its ability to adapt and perform across varying economic cycles.

Australian retail expenditure growth

Source: ABS 2025.

Strong and resilient Australian economy

The Australian economy has proven highly resilient in the face of recent global and domestic volatility, reinforcing its status as a robust and attractive destination for long-term investment capital.

A key driver of this resilience is sustained population growth, averaging around 1.7% per annum, supported by elevated levels of net overseas migration. Over the next decade, the ABS projects Australia’s population will increase from 27.4 million to 30.8 million people – a 12.4% rise or around 1.2% annually. A growing consumer base stimulates demand for retail goods and services and reinforces the role of shopping centres as essential community hubs. For well-located centres, this translates into stronger foot traffic, healthier tenant demand, and enduring relevance within local communities.

At the same time, Australia benefits from a longstanding track record of consistent retail trade growth, reflecting both the durability of household consumption and the adaptability of the sector across economic cycles. Recent data highlight this stability – according to the ABS, national retail turnover increased by 1.2% month-on-month in June 2025 (seasonally adjusted), following steady gains in May. Such outcomes demonstrate the sector’s ability to expand even in periods of elevated inflation and cost-of-living pressures.

In addition, Australia’s stable political and economic environment, coupled with transparent legal and real estate frameworks, enhances its appeal for both domestic and international investors. This low-risk profile, when combined with strong demographic and consumption trends, provides a compelling foundation for long-term investment.

Falling floor space, rising population growth and land values

Australia’s retail property market is structurally distinct from many global peers, including North America, due to its high barriers to entry and comparatively low retail floor space per capita. Australia currently provides around 0.9 square metres (sqm) of retail space per person – less than half the US average of 2.1sqm.1

This supply gap is set to widen. With population growth outpacing new retail development, retail floor space per capita is forecast to continue declining through to 2032. According to Colliers, Australia’s current shortfall of 150,000sqm in 2024 is expected to deepen to 400,000sqm by 2032. To simply maintain today’s per capita provision, an additional 2.23 million sqm of retail floor space would be required – a scenario made highly unlikely by scarce available sites in metropolitan areas, elevated building material and construction costs and restrictive development approval processes.

Planning priorities have also shifted toward residential development in response to strong population growth, further constraining the pipeline of new shopping centre projects in established locations. At the same time, rising land values are pushing new retail supply to outer urban growth corridors, where expanding populations can sustain new centres without diluting the performance of well-located, established assets.

Combined with high occupancy levels (97.6% in regional areas for example1), these dynamics create a market where demand is growing faster than supply, underpinning rental growth and long-term capital appreciation for existing shopping centre assets.

Online clicks versus bricks-and-mortar

While e-commerce has reshaped consumer behaviour globally, physical retail continues to dominate in Australia. As at June 2025, online sales accounted for just 12.7% of total retail sales2 – well below the 15.5% in the US3 and 27.8% in the UK.4

Importantly, many retailers are finding that online channels come with structural profitability challenges. High costs associated with returns and reverse logistics have encouraged a shift towards omni-channel strategies, where physical stores double as last-mile logistics hubs. According to the Australian Retailers Association, around 75% of online sales are fulfilled through omni-channel models such as ‘click and collect’, while pure-play online retailers like Amazon, eBay and Kogan represent only 25% of online transactions.

These dynamics mean in-store shopping not only remains dominant but is also more profitable, with bricks-and-mortar retailers maintaining significantly stronger EBIT margins than their online-only peers. This underscores the enduring importance of physical shopping centres as both retail destinations and critical enablers of retailers’ omni-channel strategies.

The anchor role of supermarkets

Supermarkets remain the cornerstone of shopping centre performance, serving as anchor tenants that drive reliable and consistent foot traffic. Their non-discretionary nature ensures regular visitation from local communities, creating spillover benefits for specialty retailers and service providers throughout the centre.

By contrast, centres without a major supermarket often struggle to achieve sustainable trading performance, with new developments rarely viable without at least one major supermarket anchor.

Building on this foundation, shopping centres are increasingly integrating a broader mix of non-discretionary, service-based tenants to reinforce their role as essential community infrastructure. Medical centres, allied health services, dining, and entertainment offerings are being added to enhance convenience and broaden the customer experience. This evolution strengthens tenant diversity, deepens customer engagement, and further cements the position of shopping centres as indispensable community hubs that generate resilient, recurring income streams.

Recalibration of asset values and inflated rents

Following the COVID-19 pandemic, Australia’s retail property sector has undergone a period of accelerated correction, resulting in a rebasing of asset values and recalibration of inflated rents. This adjustment has brought the sector back to more sustainable levels, positioning shopping centres for long-term growth.

Evidence of this recovery is emerging. Net income has stabilised, and listed retail REITs are reporting positive leasing spreads5, reflecting improving market confidence and healthier tenant demand.

A unique strength of the Australian retail market is the requirement for tenants to report monthly sales, giving landlords real-time insight into business performance. Importantly, the occupancy cost ratio – gross rent as a percentage of tenant sales – has been steadily declining, with the benchmark currently at 14.3%, signalling rents are now more sustainable relative to trading performance.6

According to the ABS Australian retail expenditure has historically grown at an average of ~6% per annum since 1984, without a single year of negative growth. With rents now rebased to sustainable levels, future rental growth is expected to track more closely with this long-term expenditure trend, creating a stronger alignment between tenant performance and landlord income.

At the same time, rising interest rates have lifted capitalisation rates (cap rates), placing further downward pressure on asset values. Between 2019 and 2025, while retail turnover increased 16%7, the average value of sub-regional shopping centres declined by 14%. This divergence highlights a disconnect between market fundamentals and valuations – and suggests meaningful upside potential as investor sentiment normalises and capital markets stabilise.

Countercyclical opportunity

Rising interest rates have weighed on the Australian retail property transactions market, leading to softer cap rates across all sectors. However, with the RBA cutting rates in February, May and August 2025 – and some expectations that rates will either continue to reduce further or remain stable – we believe we are near or past the bottom of the current cycle. For investors, this represents a compelling opportunity to capture value from yield compression as the cost of capital falls and buyer demand rebounds which we have already seen the early stages of.

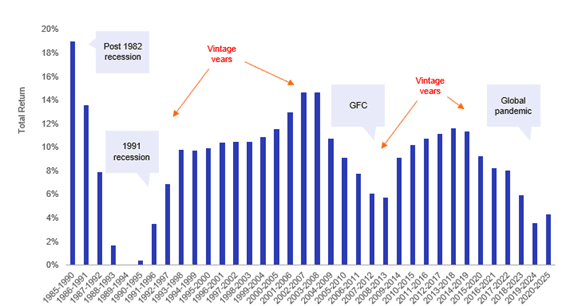

History shows that the strongest real estate returns often emerge in the early stages of recovery, following periods of muted economic activity or recession. With Australia now moving beyond the disruption of the COVID-19 pandemic, and debt markets supportive, the outlook for core real estate returns is positive.

The retail sector in particular is already leading the recovery. According to the MSCI Q2 2025 benchmark, retail recorded an annual total return of 7.8%, a significant improvement from just 0.75% in December 2023. Combined with strong economic fundamentals, persistent supply constraints, and the prospect of lower interest rates, retail real estate is well positioned to deliver outsized returns in the next phase of the cycle.

The strongest real estate returns often emerge in the early stages of recovery

A compelling long-term investment opportunity

Australian retail property presents a compelling long-term investment opportunity, supported by decades of uninterrupted retail spending growth, a resilient macroeconomic backdrop, and high barriers to new supply. Shopping centres – particularly those anchored by supermarkets and essential services – remain central to daily life, delivering consistent foot traffic and reliable income streams across economic cycles, even as e-commerce expands.

With construction costs elevated and land availability increasingly constrained, the development pipeline is limited. This supply imbalance places existing centres in a strong position to capture sustainable rental growth and long-term capital appreciation. As interest rates ease and investor confidence improves, demand for quality retail assets is increasing, positioning shopping centres as one of the most attractive countercyclical opportunities in today’s market.

We believe that well-located, actively managed retail real estate will deliver superior risk-adjusted returns over the next decade. Convenience-based centres – with higher exposure to non-discretionary spend, strong sales productivity, and low occupancy costs – are particularly well placed, reflecting both rental affordability and sustainability. In an environment of accelerating consumer and market change, deep sector knowledge and intensive asset management will be critical to unlocking value.

For more information about our real estate solutions, please get in touch.

1. Colliers Research.

2. Australian Bureau of Statistics.

3. US Department of Statistics.

4. Office of National Statistics, UK.

5. ASX – company accounts.

6. MST Marquee – the outlook for retail rents.

7. Urbis.

Important Information: This material has been prepared by MA Investment Management Pty Ltd ACN 621 552 896 AFS Representative Number 001258449 (MA Investment Management). The material is for general information purposes and must not be construed as investment advice. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer or invitation to purchase, sell or subscribe for in interests in any type of investment product or service. This material does not take into account your investment objectives, financial situation or particular needs. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. Nothing contained herein should be construed as granting by implication, or otherwise, any licence or right to use any trademark displayed without the written permission of the owner. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of MA Investment Management. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Additionally, this material may contain “forward-looking statements”. Certain economic, market or company information contained herein has been obtained from published sources prepared by third parties. While such sources are believed to be reliable, neither MA Investment Management, MA Financial Group Limited (MA Financial Group) or any of its respective officers or employees assumes any responsibility for the accuracy or completeness of such information. No person, including MA Investment Management and MA Financial Group, has any responsibility to update any of the information provided in this material.